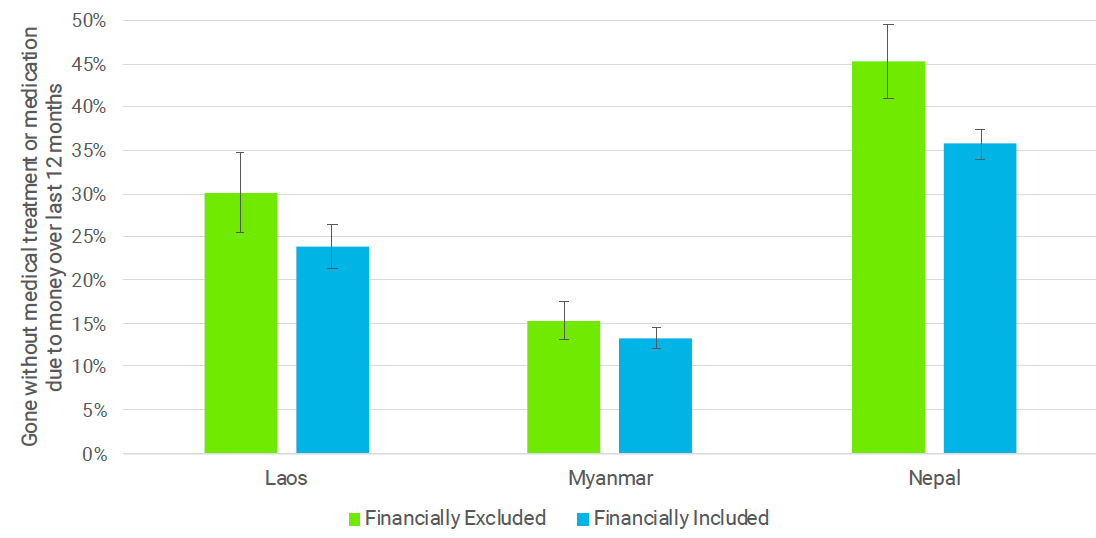

The World Bank estimates that globally, 1.7 billion adults lack access to bank accounts or other financial institutions. These unbanked adults lack access to means of savings and investing, establishing credit and borrowing, that many of us take for granted. They are disproportionately women, members of marginalized groups, and those living in rural areas and developing countries.

Governments and NGOs have undertaken substantial investments to increase financial inclusion in efforts to facilitate inclusive growth. These efforts include teaching financial literacy, setting up community savings groups, providing microfinance to small entrepreneurs, introducing mobile banking options, and other programs. Such initiatives can enable savings and reduce reliance on money lenders, increasing investments into education and entrepreneurship while decreasing gender gaps and inequality.

Although such programs offer numerous benefits, economists have struggled to fully quantify their value, a necessary step in comparing the value for money offered by alternative programs.

Traditional economic modeling approaches estimate value by considering how a savings account or loan changes one’s future earnings. But, the benefits of financial inclusion are much broader than its potential to increase incomes. Even households that do not see an increase in their eventual earnings may still benefit from access to savings and borrowing. A financially included household may be better able to afford tuition payments or deal with health expenses or economic shocks when they arrive. They may move away from living paycheque to paycheque and the insecurity that comes with it. For many financial inclusion programs, these other benefits contribute most to the value of the program.

Limestone Analytics has been developing and applying new tools to model and estimate the broader benefits of financial inclusion projects around the world. In work for World Vision Canada, Limestone applied the methods to better understand the impact of community savings groups on households in developing countries. The methods brought state-of-the-art macroeconomic and financial modeling techniques to better understand measure how community savings groups provide value to beneficiaries by relaxing constraints to savings and borrowing.

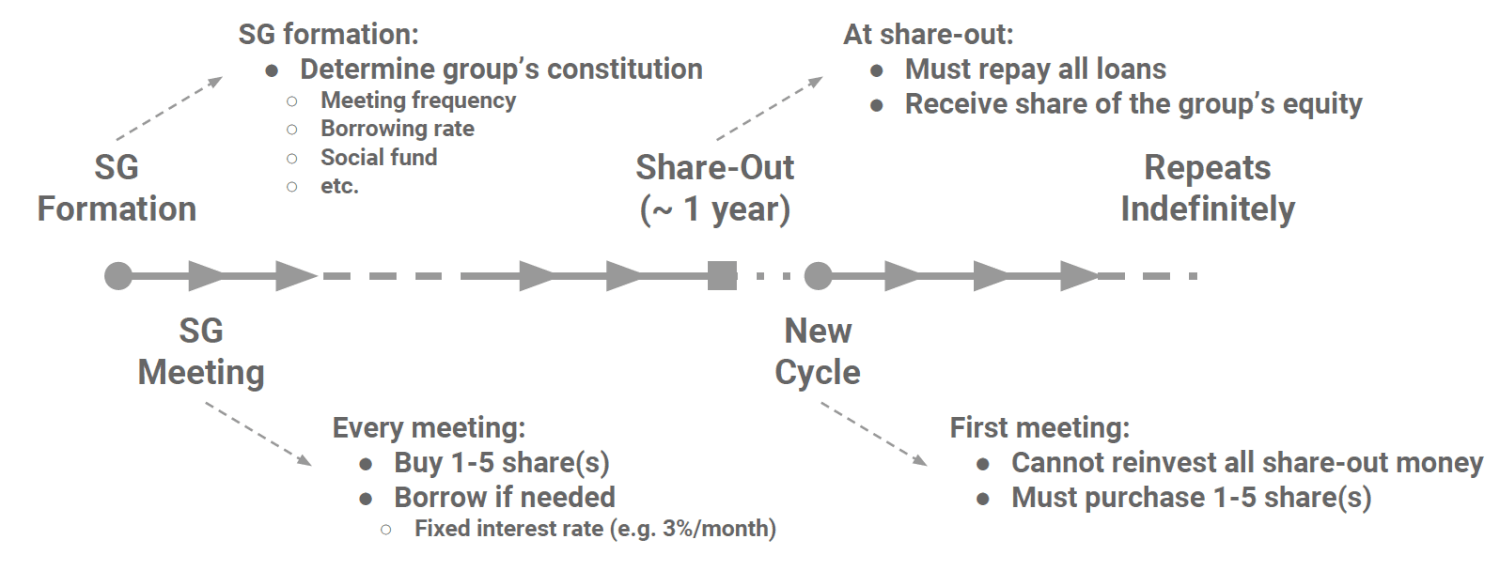

Community savings groups have been introduced by NGOs across many developing countries and have become a popular channel for savings and borrowing, particularly in more rural areas without access to more formal institutions. In a savings group, a small number of people meet regularly to contribute to a joint fund, both as a means of savings and as a means of collectively funding short-term loans to group members.

The new model adapted state-of-the-art approaches to modeling household and community income, consumption, and savings to incorporate the core features of popular savings group models. The model uses a dynamic equilibrium model with heterogeneous agents, savings, income shocks, and features from life cycle models. It is calibrated using extensive data from real world savings groups. It estimates the dollar value of savings group participation for households: how much more would a household need to earn every month to offset the disadvantage of not having access to a savings group? Researchers can use the model to assess the impact on different types of households of having access to a savings group and how changing the rules and structure of the savings group affects outcomes.

First, the analysis shows that the non-income benefits that households receive from savings groups are substantial. The consumption smoothing benefits, enabling households to better deal with income fluctuations and shocks, equal 1.38% of the value of household consumption, and can easily justify the low implementation costs of the typical savings group program.

Second, the analysis shows how borrowing and savings behaviors were impacted by different aspects of a savings group’s design. The analysis considers alternative terms that a group can adopt regarding the mandatory purchase of savings shares, the timing and interest rates for loan repayment and whether there is a share-out date when shares are returned to participants, and the group resets. Such considerations substantially impact the magnitude of the benefits, suggesting that the value households receive from savings groups depends on the design of their group. Eliminating the annual share-out date in favor of a continuous participation model, for example, more than doubles the value of the program for households.

The insights show us that the rules by which savings groups operate can significantly alter the benefits they provide to households. The results provide lessons about the most-effective design of future programs. Additionally, the methodology developed in the research provides a framework for the study of a broader set of financial inclusion instruments, allowing for the valuation of important benefits that are not usually accounted for in the cost-benefit analysis and value-for-money comparisons.

Limestone’s work in this area is at the forefront of academic research in this space. Limestone economist Frédéric Tremblay has built on this work as part of his PhD research, and the team continues to apply the methods to understand financial inclusion projects being implemented by our clients.

References:

Limestone Analytics, “Savings Groups Financial Design Report,” prepared for World Vision Canada

Tremblay, Frederic, “Savings Groups: Model, Welfare and Design,” Queen’s University Ph.D. Dissertation

World Bank, “Financial Inclusion: Financial inclusion is a key enabler to reducing poverty and boosting prosperity,” https://www.worldbank.org/en/topic/financialinclusion/overview

Photo credit: USAID / Feed the Children / Amos Gumulira